Inside DP1/26: How the PRA Plans to Transform Banking Data Collection

Credit to Oliver Hooper, Senior Solutions Consultant at Suade

On the 4th of February, the PRA released a Discussion Paper surrounding the future of Future Banking Data (FBD), which evolved from Transforming Data Collection (TDC) & Banking Data Review (BDR). This DP encourages relevant institutions to engage on the long-term strategy & approach to regulatory data collection.

The FBD programme is in place to allow the PRA to review its strategic approach to regulatory reporting for banks. It aims to deliver tangible cost reductions to catalyse competitiveness, which aligns with their secondary competitiveness & growth objective. The consensus seems to remain that availability and analysis of granular data, while increasingly being supplemented by qualitative approaches, remains vital to financial stability & the effective supervision of regulated entities.

The PRA outlined 3 key areas of potential improvement relating to data collection:

- Reviewing the content of the data.

- More carefully considering which firms they are collecting data from.

- Auditing legacy collection processes.

4 Broad Principles for FBD:

- Anchoring the data the PRA collects in its objectives.

- Collecting data “once & well” by minimising the data collected to meet its objectives but maximising its utility.

- Making it easier for firms to supply data.

- Ensuring the data collected remains fit for purpose over time.

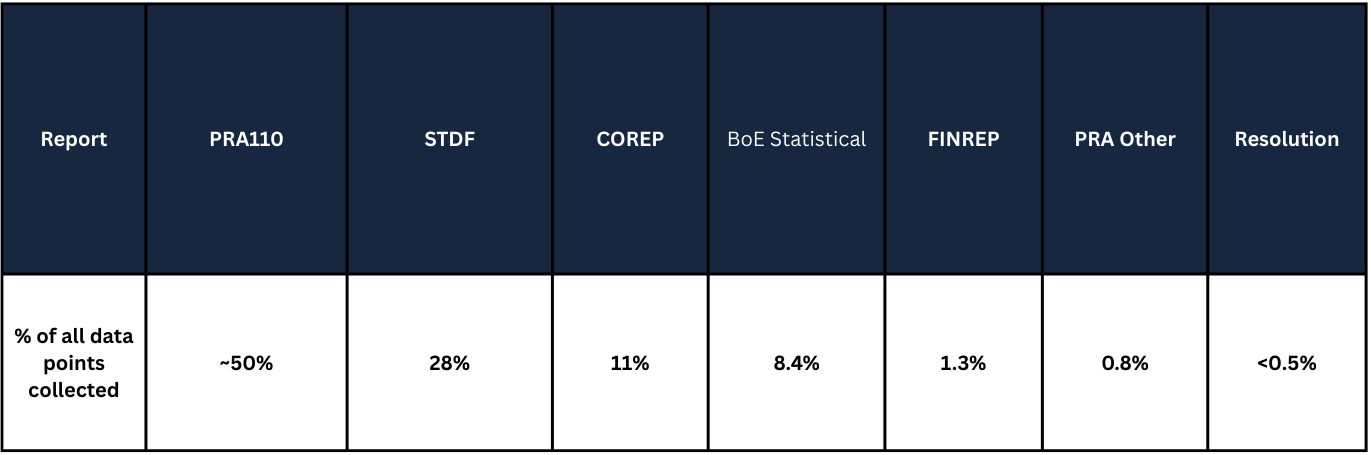

By report type, the % of data points collected can be attributed to the following regulatory returns (adapted from original metrics from the original DP):

Liquidity data points certainly make up the largest proportion of collected information.

In this DP, the PRA has also outlined a number of use cases for data collection, in alignment with their objectives & function, summarised and delineated in the sections which follow.

2. Data Collection Use Cases

Firm supervision

Regulatory data & submissions (rulebook & non-rulebook), MI, statutory transactional data, public reports and more are used to:

- Identify the appropriate risk assessment framework covering primary prudential risks e.g. liquidity, capital, operational.

- Encourage proactive supervisory engagement, using data to identify trends and improve early intervention capabilities.

- Benchmark & compare firms assisting with the identification of trends, mentioned in the previous point.

- Support proportionality & provide more tailored risk measurements for firms.

Conduct Business Model Analyses (BMA) & financial resilience assessments using ICAAPs & ILAAPs, SREPs, and regulatory returns.

Crisis supervision

Depending on the type & scale of the crisis event, different data may be requested from a variety of firm types and/or sizes. This information supports key decision-making which:

- Maintain the soundness of firms, the sector, and the broader financial landscape.

- Protect deposit holders.

- Enable orderly resolution or recovery.

- Reduce the chances of government/taxpayer intervention.

In times of crisis, the PRA seeks timely, granular datasets which can be utilised as quickly as possible, as opposed to meticulous comparability in BAU settings. It’s important that institutions have the correct infrastructure & solutions in place to make granular financial data as accessible as possible, adhering to RDARR principles & BCBS-239. While MI & aggregated information have been useful is past crises, complete, standardised granular datasets would offer timely information which is also directly comparable across firms.

Cross-sectional analysis

Across the sector & across firms, effective data collection enhances:

- Risk identification & investigation.

- Policy development & CBA.

- Research efforts.

- Financial stability monitoring.

- Thematic reviews & supervisory resource allocation.

While the PRA is exploring further qualitative approaches by using data stemming from MI & other aggregated sources, there is still a strong emphasis on the availability of granular data for cross-sectional analysis.

Clear examples of tangible use cases are outlined in the original DP for cross-firm analysis, with reference to specific report templates - mostly from FINREP & COREP.

Policy & research

Regulatory data collection further impacts the PRA’s research & policy-making capabilities, from initiation and development through to implementation and evaluation.

Research projects and historical databases e.g. HBRD should see improvement as data is further refined and gathered more effectively. For example, the HBRD has already been extended through the use of COREP & FINREP data.

Focus on the STDF

The Stress Test Data Framework (STDF) is a great example of non-rulebook granular data collection, which provides key insights into firm-specific risks & behaviour under stressed scenarios. It helps provide granular, scenario-based data which informs micro & macro-prudential policy.

Mortgage data collections

A final key focus area for targeted data collection surrounds mortgages in the UK. This is purely because this financial product constitutes a large proportion of household debt as well as banks’ balance sheets, naturally having a notable sphere of influence over broader economic conditions and financial stability. Key roles of mortgage-related data include:

- Assessment of the monetary policy transmission mechanism.

- Assessment of risk build-up from residential mortgage lending.

- Assisting the formation the supervisory methodology within the broader prudential framework.

- Aiding the execution of the BoE’s core central banking activities e.g. informing the haircut value.

- Informing a long-term macroprudential view of financial stability.

- Contribution to domestic & international agency cooperation.

3. Proposed Reforms

The PRA has identified 4 key challenges/areas for improvement:

1. Identifying existing collections which are of less value due to evolving requirements and analysis

- The PRA’s data collection spans over 400 templates of different sizes & complexity.

- The range of templates reflects regulatory changes over time.

- Similar underlying data can arise from separate templates due to different legal origins.

- Legacy data collection templates which carry less value are still in production. The PRA has started to delete templates e.g. recent FINREP deletions.

- The PRA needs to further assess which requirements are less relevant now that the UK is no longer a member of the EU.

2. Inciting clearer & more coherent collection processes.

- Potential for modernisation of data collection methods alongside BEEDS, RegData, and the FCA platform. Potential for unification of submission formats, instead of a mix of XBRL, XML, and spreadsheet submissions.

- There is also room for improvement surrounding the coordination and alignment of regulatory deadlines + collection dates. This would reduce pressure and challenges around peak submission periods.

3. Increasing clarification around PRA requirements & instructions.

- Areas of the PRA Rulebook can be tailored more towards UK requirements after Brexit.

- There are challenges around firms identifying what to submit as many requirements sit in different parts of the PRA Rulebook.

- Reporting templates and instructions inherited from the EU may still contain legacy references, meaning firms have to find the PRA’s own instructions manually.

4. Identifying & capturing new & revised data to cater for emerging risks & close existing gaps.

- There are known gaps, where new/different data are required but not actively available. A particular focus for the PRA is risk in the non-bank FI sector.

- Technological change may warrant sharper frequency of data collection & more timely submissions.

Practical steps towards reform:

The PRA refers to the 4 broad principles mentioned at the beginning of this article, aiming to address them in the context of the 4 overarching challenges, detailed above. Ultimately, taking practical steps to reform data collections will require navigation of trade-offs:

- Timeliness vs. comparability.

- Standardisation vs. flexibility.

- Aggregate vs. granular.

- Regular vs. ad hoc.

- International alignment vs. UK focus.

- Data continuity vs. decommissioning.

- Minimising rework vs. delivering improvements sooner.

It’s important for finance, data, risk, and regulatory professionals to remember the importance of the data being calculated, aggregated, and produced on a daily, monthly, quarterly, and yearly basis. There is a significant amount of value & responsibility attached to the regulatory reporting function & I believe supervisory initiatives like FBD & similar initiatives such as the BIRD project in the EU reinforce this. Additionally, it’s key to remember the PRA’s legal discretion over the request & reception of firm data at any time.

If you’re interested in finding out how Suade can help you proactively get ahead of these expectations, I’d encourage you to have a look at Suade’s financial regulatory data standard, created in conjunction with the European Commission and used as in an exemplary fashion as part of the BIRD project.